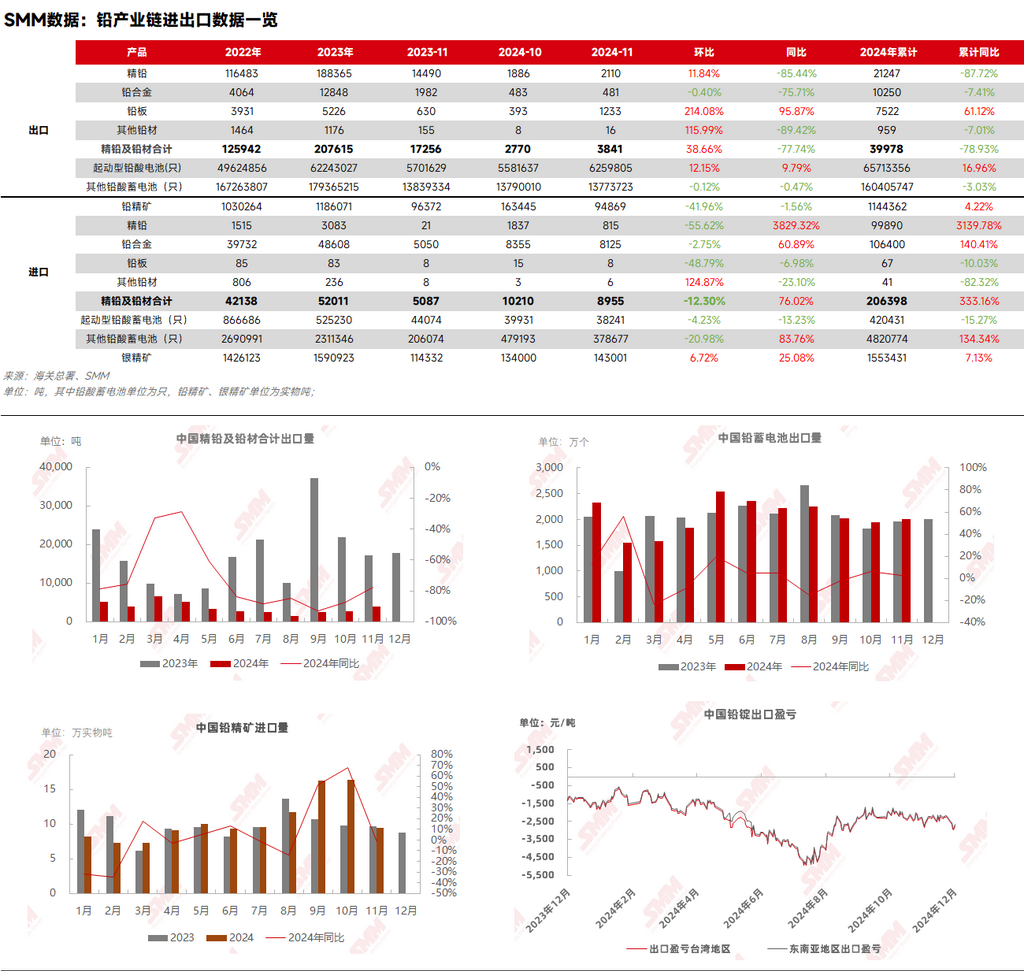

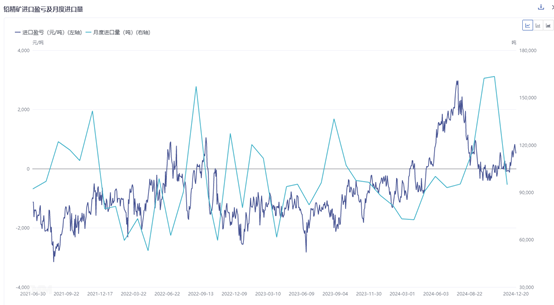

In Q4 2024, the import window for lead concentrate closed, marking the end of theoretical import profitability in the market. With smelters' H2 import orders arriving in bulk, smelters reduced procurement demand and quotations, leading to a renewed downturn in the domestic lead concentrate trading market. According to customs data, lead concentrate imports in November 2024 totaled 94,900 mt, down 41.96% MoM and 1.56% YoY. Cumulative lead concentrate imports for 2024 reached 1.1444 million mt (metal content), up 4.22% YoY.

By country, Peru, Russia, and Australia were the main sources of lead concentrate imports in November, accounting for 44.7% of the total. A trader noted that the concentrated shipment cycle of US lead-zinc mines had ended, resulting in a significant decline in lead concentrate imports from the US.

As year-end approached, some primary lead smelters, aiming to meet annual production targets, increased their procurement of silver-lead ore and polymetallic lead ore. Although these types of lead concentrate have relatively low lead metal grades, their quotations were nearly zero or negative TC. For imported ore, the trend in November silver concentrate imports differed from that of lead concentrate, recording positive growth MoM. November silver concentrate imports reached 143,000 mt, up 6.72% MoM and 25.08% YoY. In late December, the SHFE/LME lead price ratio briefly rebounded. However, as the tight supply of lead concentrate persisted, suppliers temporarily lowered pb60TC quotations. The actual import profitability of newly signed contracts for lead concentrate may fall short of theoretical breakeven levels. Smelters generally adopted a wait-and-see approach, with transactions for high-silver lead ore driven by rigid demand, while interest in purchasing low-silver lead ore remained minimal.